Most buyers focus on the loan amount they want. Lenders focus on the monthly obligation they're willing to create. FOIR is where those two perspectives meet — and understanding it before you apply will save you from both rejections and from borrowing more than your cash flow can absorb.

What FOIR means

FOIR stands for Fixed Obligation to Income Ratio. It measures what fraction of your gross monthly income is already committed to fixed repayments — existing EMIs, personal loans, car loans, credit card minimum payments — plus the new home loan EMI you're applying for.

The formula:

FOIR = (Total fixed monthly obligations ÷ Gross monthly income) × 100

If your gross monthly income is ₹1,50,000 and your existing EMIs total ₹20,000, a new home loan EMI of ₹55,000 would put your FOIR at 50%.

Where lenders draw the line

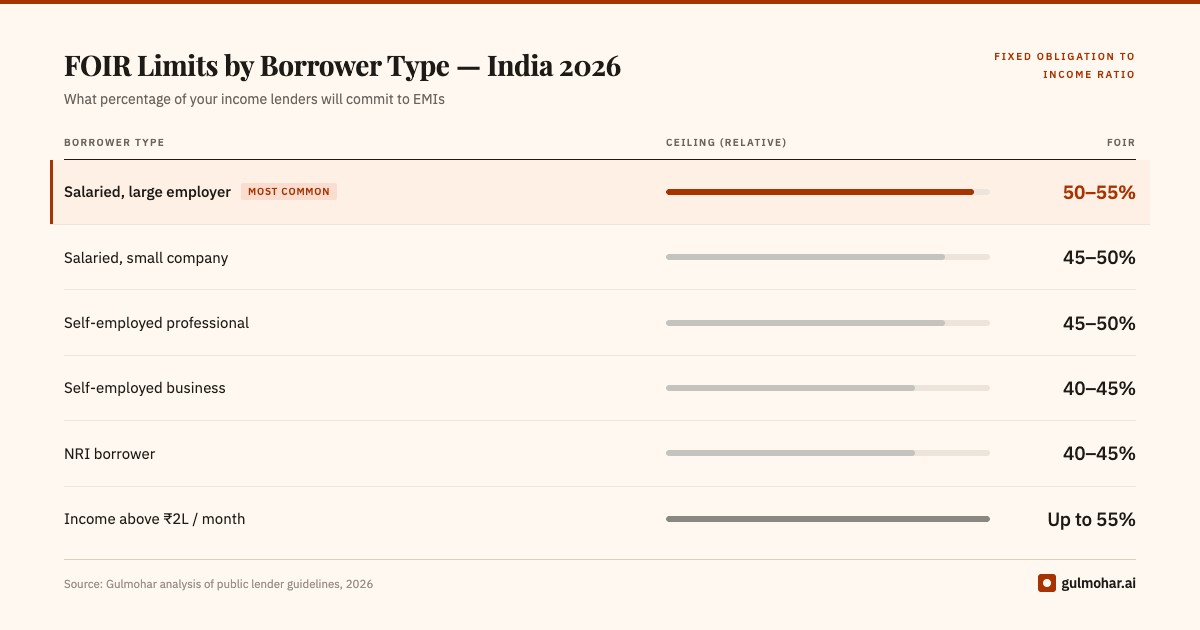

Most Indian banks and HFCs (Housing Finance Companies) cap FOIR at 40–50% for salaried borrowers. Some lenders go to 55% for high-income profiles. The practical ceiling for most borrowers:

| Borrower type | Typical FOIR cap | |---|---| | Salaried, PSU or large private employer | 50–55% | | Salaried, small or mid-size company | 45–50% | | Self-employed professional (CA, doctor, lawyer) | 45–50% | | Self-employed business owner | 40–45% | | Gross income above ₹2L/month | Up to 55% at some lenders | | NRI borrower | 40–45% |

These are indicative. Individual lenders have their own internal scorecards, and the ceiling can vary by loan amount, property type, and the lender's current risk appetite.

Breach the ceiling and the lender either rejects the application or approves a smaller loan than you requested.

The FOIR limit is applied to gross income, not take-home. Variable components — bonus, incentives, allowances — are typically weighted at 50–70% of their stated value. Build your FOIR estimate conservatively.

A worked example: why FOIR matters more than credit score

Two buyers. Same credit score (780). Same property. Same loan amount requested (₹80 lakh at 9% over 20 years — EMI approximately ₹71,980).

Buyer A: Gross monthly income ₹2,00,000. Existing obligations: car loan EMI ₹12,000, personal loan EMI ₹8,000. Total obligations with new EMI: ₹91,980. FOIR: 46%. Approved.

Buyer B: Gross monthly income ₹1,80,000. Existing obligations: car loan EMI ₹14,000, credit card limit ₹5,00,000 (lender counts 5% = ₹25,000/month). Total obligations with new EMI: ₹1,10,980. FOIR: 61.6%. Rejected, or sanctioned at a significantly lower amount.

Buyer B's problem isn't income — it's the credit card limit that they may never use but the lender is counting regardless. Reducing that limit to ₹1,00,000 drops the counted obligation from ₹25,000 to ₹5,000, cutting ₹20,000 from the obligation stack and bringing FOIR to approximately 50.5%. Borderline, but negotiable.

The hidden obligations that hurt your FOIR

Buyers routinely undercount their obligations:

- Credit card minimum payments — lenders count 5% of the total credit limit as a monthly obligation, even if you pay in full every month and carry zero balance. A ₹5,00,000 credit limit adds ₹25,000 to your monthly obligation stack.

- Loan against securities or FDs — if the EMI is fixed, it counts

- Car loans taken jointly — even if your spouse is the primary borrower, many lenders add the full EMI to your obligation stack

- Buy-now-pay-later balances — increasingly being reported to credit bureaus and included in FOIR calculations

- Personal loans from digital lenders — these show up on CIBIL even if the tenure is short

Before you apply, pull your CIBIL report and list every obligation appearing there. That is the number the lender will use — not what you believe your obligations to be.

Post-relief FOIR: the metric lenders don't tell you to track

A sharper way to evaluate your position is post-relief FOIR — what your FOIR looks like after existing loans close.

If your car loan of ₹14,000/month ends in 10 months, your FOIR in 10 months is meaningfully different. Some lenders factor this into their credit decision — particularly when the relief comes within 12–18 months of loan disbursement. More importantly, you should factor it into yours when deciding whether to prepay a loan before applying.

The maths: if prepaying ₹4,00,000 to close a loan eliminates ₹14,000/month in obligation and brings your FOIR from 53% to 45%, and the property requires an ₹80 lakh loan, the ₹4 lakh prepayment is almost certainly worth it. You preserve ₹76 lakh in borrowing capacity.

Run your property through the Gulmohar engine.

Get a full deal assessment, financial fit score, and shock simulation — not a generic verdict.

EVALUATE A PROPERTY →How to improve your FOIR before applying

These are ordered by impact, not by effort:

1. Reduce credit card limits The fastest FOIR improvement that doesn't require cash. Call your card issuer and reduce limits on cards you don't actively use. A ₹5,00,000 limit reduction saves ₹25,000 in counted monthly obligation. Do this 60–90 days before applying so it reflects on your CIBIL report.

2. Close small outstanding loans The FOIR improvement from eliminating a ₹5,000/month obligation is larger than most buyers expect — it may be the difference between a 51% and 48% FOIR, which crosses a lender threshold. If you have a personal loan or consumer durable loan with a small outstanding balance, prepay and close it.

3. Apply with a co-borrower Adding a working spouse or parent increases the gross income denominator, pushing FOIR down for the same loan amount. If your spouse earns ₹80,000/month and your combined income is ₹2,30,000, the same ₹71,980 EMI on ₹80 lakh represents a much lower FOIR against the combined income.

4. Include all legitimate income Rental income (with IT returns to support it), interest income, and professional fees can legitimately be added to the denominator. Lenders will ask for documentation — typically 2–3 years of ITRs. Income without documentation won't count.

5. Apply for a lower loan amount The blunt instrument. If FOIR is the blocker, reducing the loan request reduces the proposed EMI and brings FOIR below the ceiling. The gap can be bridged by adjusting the down payment, negotiating the purchase price, or deferring the purchase by 6–12 months while paying down existing debt.

FOIR after rejection: what to do

If a lender rejects your application citing FOIR, you have options — but none of them work immediately.

First, do not apply to multiple lenders in quick succession. Every hard inquiry appears on your CIBIL report and is visible to subsequent lenders. Multiple rejections in a short window are a compounding negative signal.

Second, identify the specific obligation driving the breach. Pull your CIBIL report and calculate which liability, if removed, brings you below the threshold. Close or reduce that obligation. Wait 60–90 days for the report to update.

Third, revisit the property. A lower purchase price means a lower loan, lower EMI, lower FOIR. If the seller is flexible or if you've found a comparable property at a lower price point, the FOIR problem may solve itself.

What this means for your evaluation

FOIR is one of five factors in Gulmohar's Financial Fit assessment. A FOIR breach caps your Financial Comfort Score at 35 regardless of other factors — because an obligation structure that leaves you with thin monthly surplus is a meaningful risk, even if the property itself is well priced.

The score doesn't just flag whether you breach the ceiling. It models your post-EMI monthly surplus, your shock resilience if income drops, and your debt service coverage at current rates versus a 150 basis point rate increase. For buyers comparing under-construction and ready-to-move options, note that your FOIR is calculated on the post-possession EMI — the pre-possession interest-only phase doesn't reduce your eligibility, but it does add carry cost that the score accounts for separately. FOIR is the starting point of that analysis, not the end.

Figures and lender thresholds are indicative based on publicly available lending guidelines as of 2026. Individual lender policies vary.