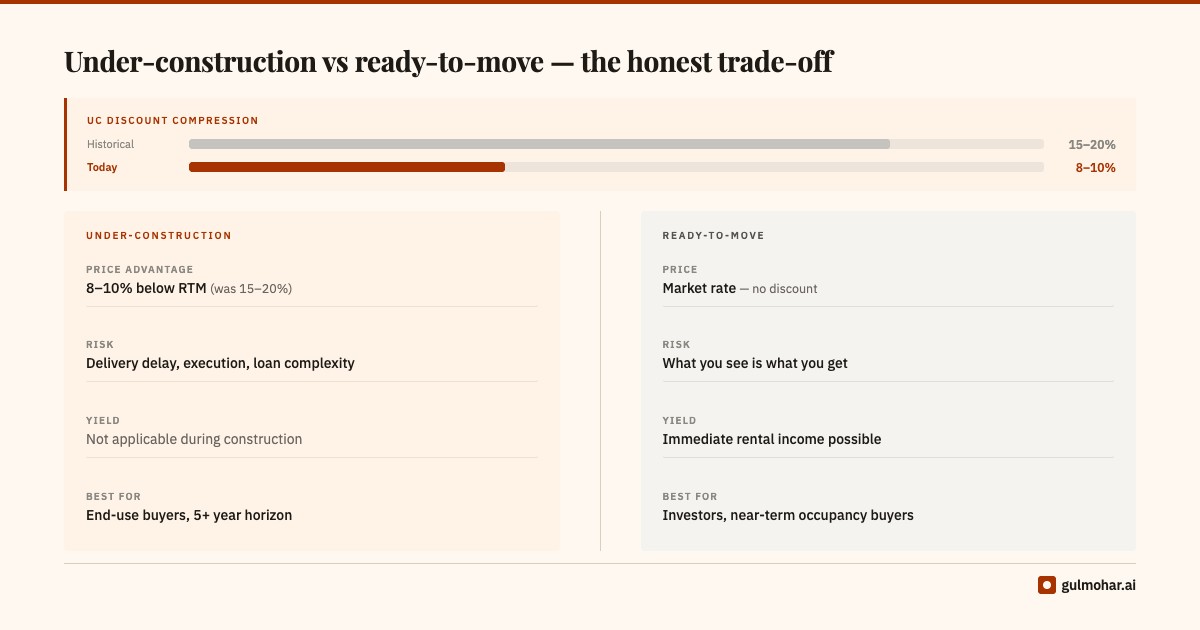

For most of the last decade, under-construction properties traded at a 15–20% discount to ready-to-move inventory. The logic was sound: you were compensating the developer for risk (theirs) and accepting execution risk (yours). In 2025–26, that discount has compressed to 8–12% in most markets, and in premium segments it has effectively disappeared.

This changes the calculus. The standard advice — "buy UC for the discount" — needs to be tested against your specific numbers rather than accepted as received wisdom.

The four costs of UC that most buyers undercount

1. Cost of carry during construction

If possession is 3 years away and you're taking a loan now, you'll be paying EMIs — either to the bank or to the developer through a construction-linked plan — while also paying rent. The total carry cost over 36 months is material.

A ₹1.2 crore loan at 9% over 3 years of pre-possession payments is approximately ₹32 lakhs in interest paid before you've moved in. Add 36 months of rent (assume ₹25,000/month) and the carry totals ₹57 lakhs.

2. GST on UC, not on RTM

Under-construction purchases attract 5% GST (or 1% for affordable housing). Ready-to-move properties — specifically those with a completion certificate — are GST-exempt. On a ₹1.2 crore purchase, 5% GST is ₹6 lakhs. This cost doesn't exist for RTM.

3. Execution risk: the cost of delay

The average delay across Indian residential projects (as tracked through RERA filings) remains 18–24 months beyond stated possession date. Model your carry cost at 4–5 years, not 3.

4. The opportunity cost of being locked in

Capital committed to a UC property is illiquid. If your financial situation changes — job change, relocation, family circumstances — extracting yourself from a UC purchase is expensive. RTM gives you optionality. UC projects also carry land title risk that only surfaces after purchase — a property title check before signing is non-negotiable for any under-construction buy.

Run the total cost model, not just the sticker comparison. A ₹1.4 crore RTM property can be cheaper in total outlay than a ₹1.2 crore UC property when carry, GST, and expected delay are priced in.

When UC still makes sense

The UC vs RTM math swings back toward UC in specific circumstances:

- Developer with a clean track record: Delivery risk is the central variable. A developer with 3+ projects delivered within 6 months of stated date is meaningfully different from the market average.

- Payment plan advantage: Some developers offer construction-linked plans where 20–30% is paid upfront and the balance on possession. This substantially reduces carry cost.

- Specific configuration: You're buying a particular floor, orientation, or unit type that isn't available in RTM inventory for the same cluster.

- Price is materially below P25 for the cluster: A genuine discount of 18%+ still justifies the risk premium.

The RTM premium is often worth paying

In a market where UC discount is 8–10% and your alternate rent is ₹25–35K/month, the RTM premium is often recovered in 24–30 months of not paying carry. For buyers who are moving in rather than investing, this is almost always the right frame.

Run your property through the Gulmohar engine.

Get a full deal assessment, financial fit score, and shock simulation — not a generic verdict.

EVALUATE A PROPERTY →A worked comparison

Abstract claims about carry costs are easier to dismiss than concrete numbers. Here's a side-by-side for a single decision a buyer might face in a typical mid-market Gurgaon or Bangalore cluster.

| | Under-construction | Ready-to-move | |---|---|---| | Sticker price | ₹1.2 crore | ₹1.35 crore | | GST (5% on UC) | ₹6 lakh | Nil | | Stamp duty + registration (~6.5%) | ₹7.8 lakh | ₹8.8 lakh | | Total acquisition cost | ₹1.34 crore | ₹1.44 crore | | Loan amount (80% LTV) | ₹1.07 crore | ₹1.15 crore | | EMI during construction (36 months) | ₹96,000/month interest-only | Not applicable | | Rent during construction (36 months) | ₹25,000/month | Not applicable | | Total carry over 36 months | ₹43.6 lakh | ₹0 | | Effective total outlay at possession | ₹1.77 crore | ₹1.44 crore |

The UC property with a ₹15 lakh lower sticker price ends up costing ₹33 lakh more over the pre-possession period — before accounting for any delay. Extend to 48 months (the realistic average including delays) and the gap widens to ₹48 lakh.

This doesn't mean UC is always wrong. It means the carry cost needs to be modelled, not ignored.

Construction-linked plans vs subvention schemes

Not all UC purchases require paying full EMIs during construction. Two payment structures change the carry cost calculation:

Construction-linked plan (CLP): You pay in tranches tied to construction milestones — foundation, slab, finishing, handover. If the developer uses the funds as they arrive, your outstanding loan balance (and therefore EMI) grows gradually. A well-structured CLP with a credible developer can significantly reduce carry versus a full loan from day one.

Subvention scheme: The developer services the interest on your loan during construction, and you begin full EMIs only at possession. These were common in 2015–19 and fell out of favour after several developers defaulted on the interest payments, leaving buyers liable for interest they thought was covered. Some developers still offer subvention; if you're considering it, verify the interest payment mechanism and what recourse exists if the developer stops paying.

The safest UC transaction is one where you pay a meaningful amount upfront (20–30%) and the balance on possession, eliminating construction-period EMI risk entirely. This structure is available less frequently, but it's worth asking for.

RTM negotiation leverage

A point that rarely appears in the UC vs RTM comparison: ready-to-move inventory often has more negotiation room. A developer or resale seller with an unsold RTM unit carries carrying costs — maintenance, property tax, loan interest if they financed the purchase. They have an incentive to close.

Under-construction projects, by contrast, typically have fixed price lists and developers who can afford to hold. A 5–8% negotiation on a ₹1.35 crore RTM property is ₹6.75–₹10.8 lakh — enough to close the sticker price gap with the UC option, while also eliminating the carry cost differential.

How we score this

Gulmohar's deal assessment includes a UC supply pipeline input — how much inventory in your cluster is under-construction — as a component of the liquidity score. High UC supply in a cluster suppresses near-term resale liquidity, which matters if your horizon is under 5 years.

The pipeline input is combined with your financial profile — your current EMI-to-income ratio, loan tenor, and surplus — to produce a stress score that accounts for what happens to your position if possession delays by 12 or 24 months. A property that looks manageable on paper often shows a different picture when modelled against a 24-month delay scenario with a 150 basis point rate increase. That's the test that matters.

Interest rates and GST figures reflect 2025–26 market conditions. Verify current applicable rates before modelling.