Of all the due diligence steps available to a property buyer, title verification is the most important and the most neglected. Buyers who skip it are not being reckless — they're usually relying on the assumption that the developer or broker has handled it, or that the bank's legal team will catch problems when processing the loan. Both assumptions have limits that can cost you the property.

What "clear title" actually means

A clear title means:

- The seller (or developer) has legal ownership of the property — verified through a chain of documents going back at least 30 years

- The property is free of encumbrances — no loans, charges, or liens registered against it

- There are no pending litigations related to the property or the land in any court

- The relevant government approvals are in order — building plan sanction, occupancy certificate (for ready-to-move), or RERA registration (for under-construction)

"Clear title" does not mean "the seller claims ownership." It means an independent legal verification has confirmed the chain of title is sound through original documents — not through representations from the party selling you the property.

Why the bank's legal check isn't enough

When you take a home loan, the bank conducts its own legal review before disbursing funds. Many buyers treat this as a proxy for independent due diligence. The problem is structural: the bank's interest is in the security of its lien, not in protecting your ownership claim.

The bank's lawyer is asking: "Can the bank enforce its mortgage if the borrower defaults?" That is a different question from: "Is this buyer's title clean and defensible?" A bank can have a perfectly enforceable mortgage on a property with a contested title — the bank's security is its priority charge over the asset, regardless of who has the better ownership claim.

Banks have approved loans on properties that subsequently turned out to have title defects. In those situations, the bank is protected by its first charge; the buyer is left holding a disputed asset.

A bank-approved loan does not mean the title is clean. Always commission an independent title search from an advocate who represents your interests, not the lender's.

What an encumbrance certificate tells you — and what it misses

The Encumbrance Certificate (EC) is issued by the Sub-Registrar's office and lists all registered transactions and charges against the property over a specified period. Request an EC for the maximum available period — typically 30 years — and review it for:

- Prior mortgages or charges that should have been discharged but still appear on record

- Court attachments or government acquisition notices

- Prior sale registrations from the same seller to a different buyer (rare but it happens, particularly with agricultural land conversions)

The EC is a starting point, not a complete picture. It captures only registered transactions. Unregistered interests are invisible on an EC. Specifically:

- Family disputes and succession claims — a legal heir who did not consent to a sale can challenge it years later; this won't appear on an EC

- Power of attorney complications — if any link in the title chain involved a sale by power of attorney, the validity of that PoA needs separate verification

- Agricultural land conversion irregularities — in peri-urban areas where farmland has been converted to residential use, the conversion order itself may have been challenged or improperly obtained

- Pending partition suits — co-ownership disputes filed in civil courts don't automatically appear in Sub-Registrar records

This is why an EC alone is insufficient. You need an advocate who searches not just registration records but also court records for the specific survey numbers involved.

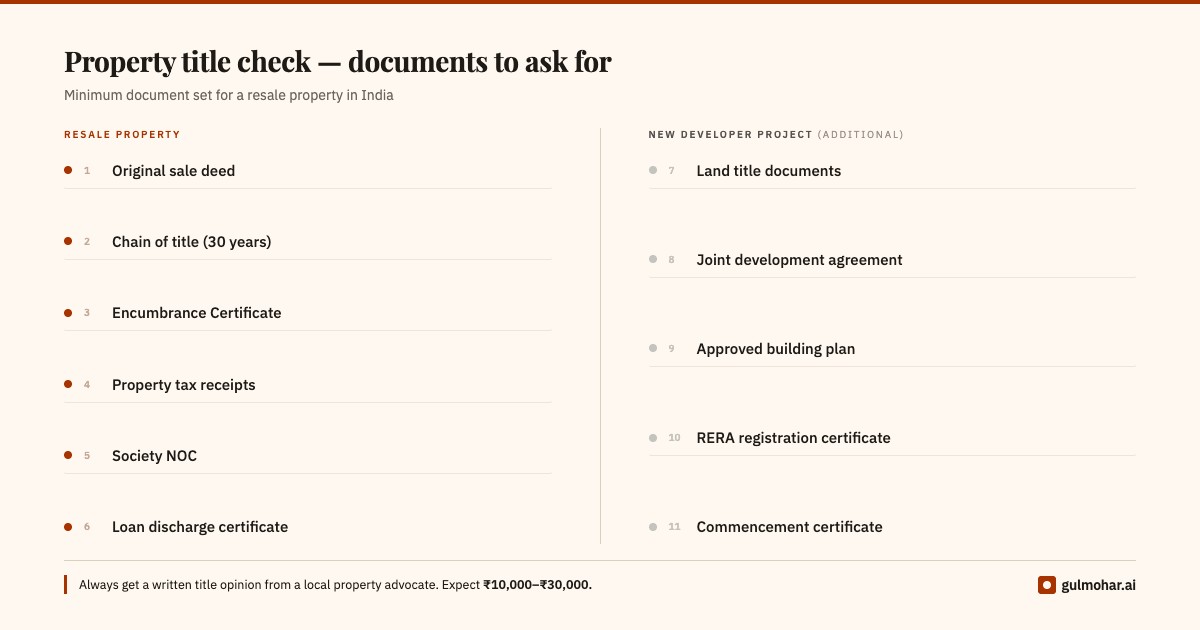

The documents to ask for

For a resale property, the minimum document set you should review:

- Original title deed / sale deed — the document that transferred ownership to the current seller

- Chain of title documents — the previous 2–3 sale deeds establishing the ownership chain back 30 years

- Encumbrance Certificate — for the past 15–30 years from the Sub-Registrar's office

- Property tax receipts — the most recent 3–5 years; confirms possession and absence of government revenue disputes

- NOC from housing society — if applicable, confirms no dues outstanding

- Loan NOC / discharge certificate — if the seller had a mortgage on the property, a no-dues certificate and release deed from the lender is mandatory; without this, the lender's charge continues against the property

For a new project from a developer, additionally:

- Land title documents — the developer's ownership deed or development rights agreement for the specific survey numbers

- Joint development agreement — if the developer is building on a landowner's land, the JDA must explicitly grant the developer authority to sell units and collect payments from buyers

- Approved building plan — the sanctioned plan from the local authority, not just an architect's drawing

- RERA registration certificate — and the underlying project details on the portal (see our separate guide on RERA verification)

- Commencement certificate — in states where required, confirms the developer had legal authority to begin construction

Run your property through the Gulmohar engine.

Get a full deal assessment, financial fit score, and shock simulation — not a generic verdict.

EVALUATE A PROPERTY →Who should do the verification

Use an advocate who specialises in property law in the specific state where the property is located. Property law in India is substantially state-specific — stamp duty rates, registration procedures, specific document requirements, and common encumbrance patterns all vary. A lawyer based in Delhi handling a Bangalore property transaction will miss things a local Bangalore property advocate would catch as a matter of routine.

The advocate should provide a written title opinion covering:

- Each document in the title chain and any gaps or irregularities

- Encumbrance status and whether any charges appear discharged or pending

- Court search results for the relevant survey numbers

- Specific risks identified and the advocate's assessment of their severity

- A clear statement on whether the title is clean enough to proceed

Expect to pay ₹10,000–₹30,000 for a thorough title opinion in a major city. For high-value properties (above ₹1 crore), paying at the higher end for a senior advocate with specific transactional experience is worth it. This is not the place to optimise for cost — a title defect discovered after registration requires litigation to resolve, which is orders of magnitude more expensive.

Do not accept verbal assurances. An advocate who is unwilling to provide a written opinion is an advocate whose opinion isn't worth much.

What happens if a title problem is found

If the title check surfaces a problem, you have options — none of them fast:

Negotiate a price reduction — if the defect is curable (an outstanding discharge certificate, a missing link in the chain), the seller can be asked to resolve it before the transaction closes. This is the cleanest outcome.

Walk away — if the defect is material (disputed succession, unresolved litigation, conversion irregularity), the prudent choice is to not proceed. The earnest money negotiation is uncomfortable; the alternative is worse.

Obtain title insurance — a small number of insurers offer property title insurance in India. Coverage is limited and the product is not yet mature, but for high-value transactions with a specific, identified risk, it is worth asking your advocate about.

Do not proceed with a purchase after a negative title opinion in the hope that the problem won't surface. The probability of it surfacing at the worst moment — when you are trying to sell — is high enough that the risk is not worth taking.

What Gulmohar's risk score includes

Our risk assessment includes a legal flag indicator — whether the property has RERA registration for under-construction projects (how to verify RERA status), whether the developer has known litigation against them, and whether the project appears in distressed property databases. This is a structured screening signal, not a substitute for independent legal verification.

What the Gulmohar score is good for: flagging that a closer look is warranted before you invest time and money in a title check. What it cannot do: replace the advocate's review of original documents. Use the score to prioritise; use the advocate to verify.

This article covers general principles of title verification in India. Requirements vary significantly by state. Always obtain independent legal advice specific to your property and jurisdiction.