Whitefield's transformation from an IT suburb into Bangalore's second CBD has been genuine. The Purple Line metro, ITPL Phase 2, and a decade of commercial development have structurally changed the corridor. But the appreciation that followed — roughly 45–60% across the corridor between 2021 and 2024 — has created a wide dispersion of outcomes: some clusters remain rational, others are priced for a future that may take longer than buyers expect.

The corridor is not one market

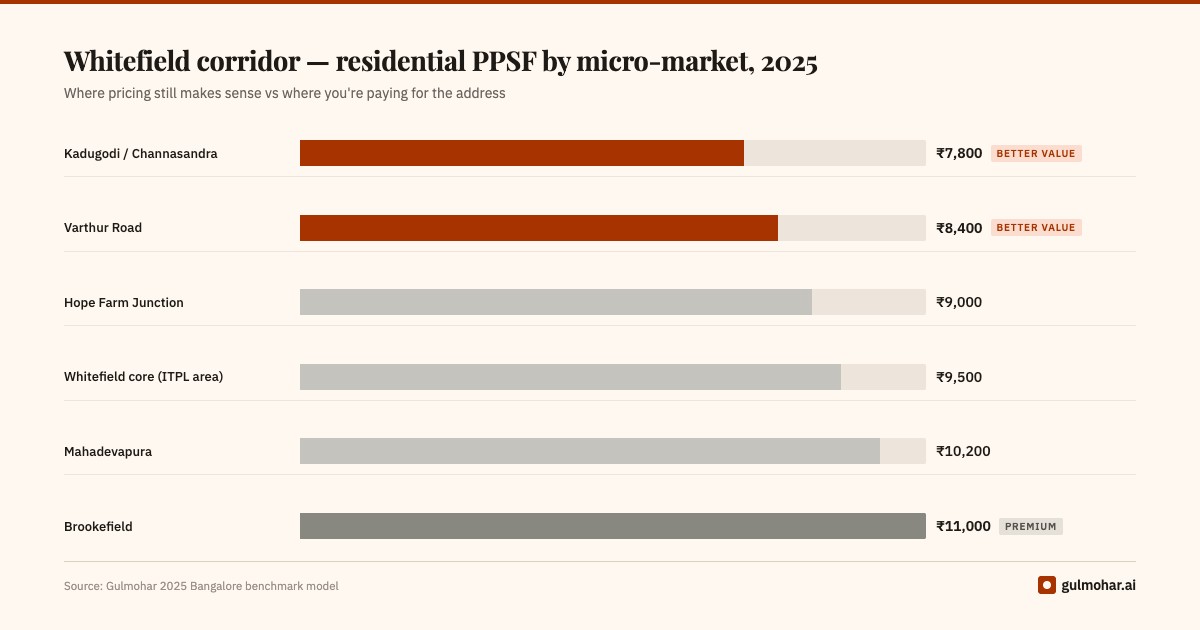

A common mistake is treating "Whitefield" as a uniform location. The corridor spans from Marathahalli in the west to Varthur and Sarjapur Road in the east — a distance of 18–22km — with dramatically different pricing, infrastructure, and liquidity at each node.

Marathahalli and Outer Ring Road junction is the corridor's most liquid end. Median PPSF on SBA runs at ₹8,500–₹10,500. Resale depth is good; this is where buyers with a 3–5 year horizon can sell without significant price concession. The downside: traffic congestion and the infrastructure isn't keeping pace with density.

ITPL / Whitefield main has appreciated the most. Median PPSF now sits at ₹11,000–₹14,000 for apartments. The metro connectivity (Whitefield station on the Purple Line) is real and has been priced in. At current levels, yield compression is significant — gross yields have fallen to 4.2–4.8% for residential.

Varthur / Sarjapur Road offers the corridor's most compelling entry point for long-horizon buyers. Median residential PPSF around ₹8,000–₹9,500, infrastructure is improving (the Outer Ring Road extension and planned metro extensions), and UC supply is manageable relative to demand depth. The trade-off: commute friction is real today, and appreciation is a multi-year thesis.

Gross yield calculation: (Annual rent ÷ Total purchase cost) × 100. "Purchase cost" should include stamp duty, registration, and any GST — not just the agreement value. Many quoted yields use agreement value only, which overstates the actual return.

The under-construction pipeline concern

One number that should inform any Whitefield purchase decision: the UC-to-RTM ratio. Across the corridor, approximately 52% of listed inventory is under-construction. In some pockets — particularly Sarjapur Road and Varthur — it's 65%+.

High UC supply is a liquidity depressant. When your 3-year-old RTM apartment comes to market in 2028, it will be competing with a wave of new possessions from projects launched in 2024–25. Price your exit assumptions conservatively if you're in a high-UC-density cluster. A similar dynamic is playing out in the NCR — Gurgaon sector pricing shows the same UC discount compression across most clusters.

Developer quality varies sharply

The Whitefield corridor has attracted both premium pan-India developers and smaller local builders. The delivery track record dispersion is significant. Projects from established developers (Prestige, Sobha, Puravankara) have substantially better completion rates than smaller players in the same clusters. Pay the developer premium — it's not a brand tax, it's execution risk insurance.

Run your property through the Gulmohar engine.

Get a full deal assessment, financial fit score, and shock simulation — not a generic verdict.

EVALUATE A PROPERTY →The rental market and what it tells you about pricing

Rental yields are a useful reality check on whether a market's price appreciation has been demand-driven or speculative. In the Whitefield corridor, the picture is mixed.

In ITPL / Whitefield main, a 2BHK of 1,100–1,200 sqft commands ₹28,000–₹38,000/month in rent. At a purchase price of ₹1.3–1.5 crore for a comparable unit, gross yield works out to roughly 2.4–3.5% before costs. That is below the risk-free rate available on fixed income instruments, which means buyers are implicitly pricing in capital appreciation to justify the investment. That's a legitimate thesis — but it needs to be explicit, not assumed.

In Varthur / Sarjapur Road, a 2BHK of similar size rents at ₹22,000–₹30,000/month. Purchase price at ₹95 lakh–₹1.15 crore gives gross yields of approximately 2.8–3.8%. Marginally better, still requiring an appreciation thesis, but with more realistic entry pricing.

Marathahalli offers the best yield profile of the three sub-markets: rents of ₹25,000–₹35,000 against lower purchase prices produce gross yields closer to 3.2–4.2%. The liquidity depth here also means a shorter void period between tenants.

These are gross yields before property tax, maintenance, vacancy, and brokerage. Net yields run 25–40% below gross depending on the project's maintenance cost structure. For a ₹1.2 crore property with 10 months of occupancy annually, add ₹18,000–₹24,000/year in maintenance charges and ₹10,000–₹15,000/year in property tax. The net yield picture is materially different from the gross.

The stamp duty and registration cost that most buyers undercount

Karnataka levies stamp duty at 5% on residential properties above ₹45 lakh, plus registration fees of 1% (capped at ₹1.5 lakh from April 2025). For a ₹1.2 crore purchase in the Whitefield corridor, that's ₹6 lakh in stamp duty and ₹1.2 lakh in registration — ₹7.2 lakh in transaction costs that are immediate and irrecoverable.

These costs matter when calculating your effective entry price for yield or appreciation calculations. A property that looks attractive at ₹1.2 crore sticker cost is actually a ₹1.27 crore entry — which changes the yield and breakeven calculus.

What a fair price looks like today

For a 2BHK in the ITPL / Whitefield main zone:

- Below ₹11,000 PPSF SBA: likely below the P25 benchmark — worth investigating why

- ₹11,000–₹13,500 PPSF: fair to moderately premium depending on floor and project specification

- Above ₹14,000 PPSF: you're paying a significant premium that needs to be justified by specific features or the particular project

For Varthur / Sarjapur Road, the equivalent brackets are ₹7,500 / ₹7,500–₹9,500 / above ₹10,000. For Marathahalli / ORR, ₹8,000 / ₹8,000–₹10,500 / above ₹11,000.

These figures should be tested against the specific cluster and asset class — aggregate corridor benchmarks mask significant within-cluster variation.

How to evaluate a specific listing

When you're looking at a specific property in the corridor, four checks before you visit:

Verify the RERA registration on the Karnataka RERA portal (rera.karnataka.gov.in) for any under-construction project. Confirm the registered completion date, check the developer's complaint history, and compare the approved unit count to what's being sold. A project that is selling more units than registered is a red flag.

Check the carpet-to-SBA ratio. Whitefield projects vary widely — loading factors between 1.20x and 1.42x are common. A unit quoted at ₹12,500 PPSF on SBA with a 1.38x loading factor costs ₹17,250 PPSF on carpet — a meaningfully different number than a ₹13,000 PPSF quote with a 1.22x loading.

Understand the maintenance regime. Premium projects in ITPL / Whitefield main carry maintenance charges of ₹4–8/sqft/month. On a 1,400 sqft apartment, that's ₹67,000–₹1.35 lakh annually — a real cost that affects both your holding cost and the rental yield calculation.

Ask about the possession timeline explicitly. For UC projects, ask for the RERA-registered completion date and the developer's internal target. The gap between these two is informative. Developers with good track records typically quote internal targets within 3–6 months of the RERA date. A developer quoting 18 months ahead of the RERA date is, in effect, telling you to expect a delay.

Benchmark data based on Gulmohar's model covering RERA registrations, active listings, and transaction data for Bangalore East. Figures are indicative as of Q1 2026.